The Ultimate Guide to Private Student Loan Refinancing

This guide provides you with the tools, insights, and strategies required to manage your student loans and carve a clear path toward financial freedom.

Student loan refinancing involves multiple considerations that can feel overwhelming. This guide breaks down the process and provides practical strategies to help you effectively manage your student loan debt. Whether you want to reduce monthly payments, save money over time, or pay off loans more quickly, you’ll find the information needed to make smart financial decisions that match your specific goals.

By sharing the knowledge and tools needed to make educated decisions, we can help you take control of your financial future.

- Why Should You Consider Strategic Student Loan Refinancing for Your Financial Freedom?

- What Is INvestEd—and Why Should You Trust Them with Your Student Loan Refinancing?

- What Exactly Is Student Loan Refinancing?

- What Are the Benefits of Refinancing Student Loans?

- What Are the Steps to Follow in the Student Loan Refinancing Journey?

- How Does INvestEd Guide You Through the Refinancing Process?

Why Should You Consider Strategic Student Loan Refinancing for Your Financial Freedom?

Refinancing your student loans can be a smart way to improve your financial situation. In this section, we’ll explore why strategic student loan refinancing is often a key step in achieving financial stability, as it can open the doors to a world of benefits that extend far beyond immediate savings.

How Can Lower Interest Rates Transform Your Long-Term Savings?

At its core, student loan refinancing offers you the opportunity to exchange high-interest rates for more favorable ones. The significance of this cannot be overstated. By securing a lower interest rate through refinancing, you’re poised to save a substantial sum of money over the life of your loans.

Even a small reduction in interest rates can result in significant savings over time. For each percentage point your rate drops, you could potentially save thousands of dollars across the lifespan of your loan. This is particularly impactful for borrowers with substantial loan balances or longer repayment terms.

Will Refinancing Reduce Your Monthly Student Loan Payment Burden?

Are student loan payments straining your budget, or are you ready to pay them off faster? Refinancing addresses both scenarios by giving you two paths: you can lower your monthly payments for immediate relief, or you can shorten your loan term to eliminate debt sooner.

When you refinance to a lower interest rate, your monthly payment usually decreases, even if you maintain the same loan term. Refinancing also offers you the option to choose shorter loan terms, which reduces the total interest you’ll pay over the life of the loan while helping you become debt-free sooner.

By refinancing to a shorter term, you might see a slight increase in your monthly payments, but the acceleration in loan payoff and the reduction in total interest can be substantial. For instance, refinancing a $40,000 loan from a 20-year term to a 10-year term would help you become debt-free a decade earlier, potentially saving you thousands in interest payments along the way. Of course, securing a lower interest rate may also make this possible, even with a smaller monthly payment.

Many borrowers find this approach particularly appealing as they progress in their careers and their income increases. The ability to eliminate student debt faster opens up opportunities to focus on other financial goals, such as homeownership, starting a business, or building wealth through investments.

What Are the Potential Savings Over the Life of Your Refinanced Student Loan?

Let’s put this into perspective: the savings potential of strategic student loan refinancing can amount to thousands of dollars. For borrowers with significant loan balances or high interest rates, the savings can easily reach five figures or more.

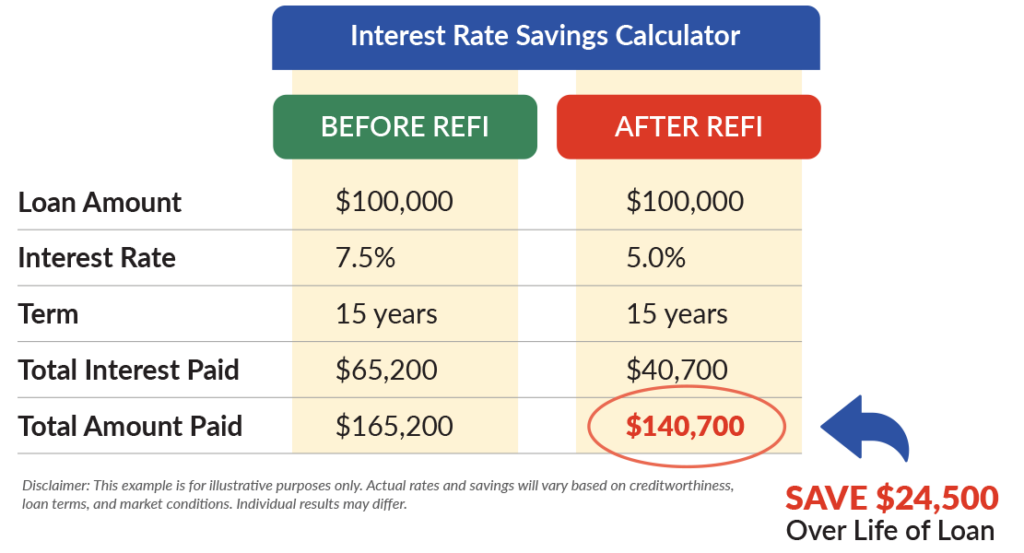

Consider a borrower with $100,000 in student loans at a 7.5% interest rate on a 15-year term. By refinancing to a 5% interest rate, they could save approximately $24,500 over the life of the loan. And for the many borrowers facing double-digit interest rates today—with many loans in the 11-13% range—the potential savings would be even more substantial. Such savings could then be directed toward building an emergency fund, buying a home, or investing in retirement. It’s an opportunity to convert debt into wealth-building power, especially for those currently paying the highest rates.

However, strategic refinancing is not a one-size-fits-all solution. The key is to understand how to wield this powerful tool effectively and make sure it aligns with your unique financial goals and circumstances. In the following sections of this guide, we will walk you through the process.

What Is INvestEd—and Why Should You Trust Them with Your Student Loan Refinancing?

When it comes to private student loan refinancing, having a knowledgeable and experienced ally by your side can make all the difference. INvestEd is a name synonymous with expertise, trustworthiness, and a relentless commitment to your financial well-being.

For more than 40 years, INvestEd has been Indiana’s trusted free expert resource for students and parents navigating the complex journey of higher education financing. Our mission has always been clear: help Hoosier families maximize free money for college and graduate with the least debt possible.

Our team assists families at every stage—before, during, and after college—providing friendly, expert financial aid guidance at over a thousand events each year, as well as over the phone, online, and via email.

We understand that sometimes, even after exhausting all other aid options, high-rate loans may be necessary to complete your education funding. That’s why the INvestEd Refi Loan was specifically designed to help borrowers escape these costly loans and transition to more manageable repayment terms after graduation. We are committed to supporting Hoosiers throughout their entire educational journey.

What Experience Does INvestEd Bring to Your Refinancing Journey?

With decades of experience in the industry, INvestEd has guided thousands of borrowers through economic booms, recessions, and everything in between, developing the kind of expertise that can only come from years of dedicated service in this specialized field.

Our journey has been marked by countless success stories, where borrowers like you have harnessed the power of refinancing to transform their financial futures. From recent graduates managing entry-level salaries while tackling significant loan burdens to established professionals seeking to optimize their remaining education debt, we’ve provided tailored solutions that address the unique challenges each borrower faces.

Why Should You Trust INvestEd with Your Student Loan Refinancing Needs?

INvestEd has earned its reputation as a trusted resource for those navigating the labyrinth of student loan refinancing. We’re not just here to provide information; we’re here to empower you with the knowledge and insights needed to make well-informed decisions that align with your financial goals.

Our commitment to transparency sets us apart in the industry. We don’t just highlight the benefits of refinancing; we openly discuss potential trade-offs and considerations to ensure you have a complete picture. Our advisors take the time to understand your unique financial situation, explaining options in clear, jargon-free language so you can make confident decisions.

Navigating student loan refinancing can be daunting, but you don’t have to embark on this journey alone. Our team of experts at INvestEd is dedicated to being your guiding light. We’re more than advisors; we’re partners in your financial success. Every step of the way, we’ll be there to demystify the process, answer your questions, and provide you with tailored strategies that make a tangible difference.

What Exactly Is Student Loan Refinancing?

Student loan refinancing is not just a financial transaction; it’s a financial strategy that can redefine your economic future. In this section, we’ll dive deep into the concept of student loan refinancing, exploring its definition and the myriad benefits it offers to borrowers seeking a brighter financial horizon.

How Does Student Loan Refinancing Work to Transform Your Debt?

Student loan refinancing is the art of seizing control over your student loan debt. It involves replacing one or more of your existing student loans with a new loan, ideally one that offers more favorable terms, most notably a lower interest rate.

When you refinance, a private lender pays off your existing loans and issues you a new loan with new terms. This process allows you to combine multiple loans into a single loan, potentially with a lower interest rate, different repayment term, or both. The result is a simplified loan structure that aligns better with your financial goals and circumstances.

The refinancing process typically begins with an application that evaluates your creditworthiness, income, and other financial factors. Based on this evaluation, lenders determine whether to approve your application and what terms to offer. Once approved and accepted, the new lender pays off your existing loans, and you begin making payments on your new refinanced loan.

This financial maneuver empowers you to reshape your student loan landscape, potentially reducing your monthly payments, decreasing the total interest paid, and even accelerating your journey to debt freedom.

What Are the Benefits of Refinancing Student Loans?

How Can Refinancing Save You Thousands in Interest Payments?

At its core, student loan refinancing is about reducing the cost of your education. By securing a lower interest rate, you can potentially save thousands of dollars over the life of your loans. This translates into money back in your pocket, money that can be invested, saved for life’s milestones, or simply enjoyed without the burden of high-interest payments.

For example, a borrower with $60,000 in student loans at an 11% interest rate on a 10-year term would pay over $39,000 in interest over the life of the loan. By refinancing to a 6% interest rate, the interest paid would drop to approximately $19,900—a savings of $19,100.

While private student loan interest rates can vary significantly, with advertised ranges extending up to 18.99% as of June 2025, it’s important to understand that the lowest rates in any lender’s range typically include available discounts—such as a 0.25% reduction for enrolling in automatic payments—and are reserved for borrowers with exceptional credit profiles. The majority of borrowers qualify for rates in the upper portion of a lender’s rate range.

Even a 1% reduction in your interest rate can lead to significant savings, particularly for larger loan balances. These savings compound over time, potentially amounting to tens of thousands of dollars saved for those borrowers with substantial student loan debt.

How Does Refinancing Simplify Your Monthly Repayment Process?

Managing multiple student loans with different interest rates and due dates can be akin to juggling flaming torches. Refinancing simplifies this complexity by consolidating your loans into a single, more manageable monthly payment.

This streamlined approach eliminates the need to track multiple payment deadlines, reducing the risk of missed payments that could damage your credit score. It also provides a clearer picture of your student loan obligation, making it easier to budget and plan for the future.

Additionally, working with a single lender means having one point of contact for any questions or concerns about your loan. This simplified administrative experience can save you time and reduce the frustration often associated with managing multiple loan servicers.

Can Refinancing Help You Pay Off Your Loans Faster?

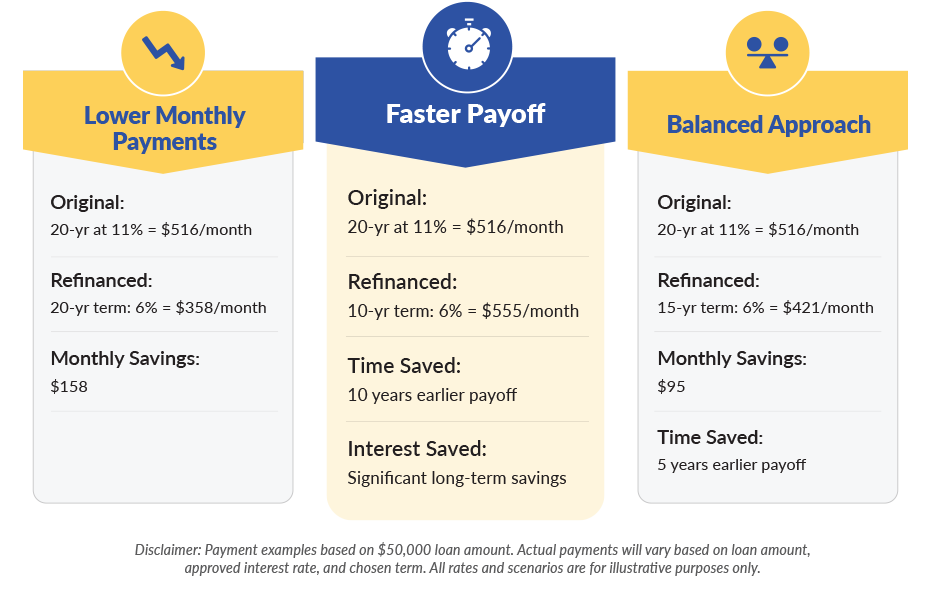

Are you eager to bid farewell to your student loans sooner? Through refinancing, you can choose a shorter loan term, which not only accelerates your path to debt freedom but can also lead to even greater interest savings.

For instance, refinancing from a 20-year term to a 10-year term will increase the amount of your monthly payments, but significantly reduce the amount of time you’re in debt and the total interest you pay over the life of the loan. This approach can be particularly valuable for borrowers who have experienced income growth since taking out their original loans.

Some borrowers choose to maintain the same monthly payment amount after refinancing to a lower interest rate, effectively paying extra toward principal each month. This strategy can help you pay off your loans months (or even years!) ahead of schedule without affecting your monthly budget.

But remember, not all student loan refinancing opportunities are created equal. To maximize these benefits, you need to take a strategic approach.

What Are the Steps to Follow in the Student Loan Refinancing Journey?

In this section, we cover the entire refinancing process, illuminating each step with insights and expertise to ensure that you’re equipped to make informed decisions.

How Do You Properly Assess Your Current Loan Situation?

Our journey begins with a thorough assessment of your existing student loans. This critical first step lays the foundation for all refinancing decisions to follow. To properly evaluate your current loan landscape, you’ll need to gather comprehensive information about each of your existing loans.

Start by creating a detailed inventory of all your student loans. For each loan, record the following essential information:

- Current loan balance: The precise amount you still owe on each loan

- Interest rates: The rate you’re paying on each loan

- Loan types: Whether they are federal (subsidized, unsubsidized, PLUS, etc.) or private loans

- Repayment terms: The length of your current repayment period and how many years remain

- Monthly payments: The amount you pay each month toward each loan

- Loan servicers: The companies that currently manage your loans

For federal loans, you can access this information through the National Student Loan Data System (NSLDS) or your studentaid.gov account. For private loans, review your loan statements or online account portals, or contact your loan servicers directly.

Pay particular attention to loans with higher interest rates, as these are typically prime candidates for refinancing. For federal loans specifically, consider whether federal loan consolidation through the Department of Education might be beneficial. Federal loan consolidation is a process that combines multiple federal loans into a single Direct Consolidation Loan while maintaining all federal benefits and protections. Also make note any special benefits attached to your federal loans, such as income-driven repayment plans or potential loan forgiveness options, as these will be important considerations in your refinancing decision.

How Can You Define Clear Financial Goals for Your Refinancing Strategy?

With your current loan landscape in focus, it’s time to define your financial goals. Clear objectives will serve as the compass that steers your refinancing strategy and aligns each decision with your aspirations. You must first consider what you hope to achieve through refinancing.

Are you primarily seeking to reduce your monthly payments to ease cash flow constraints?

This goal might be particularly relevant if you’re early in your career, facing other financial obligations, or experiencing temporary financial challenges. In this case, you will focus on refinancing options that offer lower interest rates, but also extend repayment terms.

Is your primary aim to save money in the long term by reducing the total interest paid over the life of your loans?

If you’re financially stable and looking to minimize the overall cost of your education, you might prioritize refinancing options with the lowest possible interest rates, even if it means maintaining or slightly increasing your monthly payments.

Are you determined to become debt-free as quickly as possible?

If accelerating your loan payoff is your priority, you’ll focus on refinancing options with shorter terms, which typically come with higher monthly payments but lead to faster debt elimination and less total interest paid.

Or perhaps you’re seeking a balance of these objectives—lower monthly payments along with moderate long-term savings? In this case, you might look for refinancing options that offer a better interest rate while maintaining a similar loan term.

Your financial goals may also be influenced by other life objectives. Are you saving for a home purchase, planning to start a family, or building retirement savings? Consider how student loan refinancing fits into your broader financial picture and long-term plans.

Be specific about your priorities and, if possible, quantify your goals. For example: “I want to reduce my monthly payment by at least $200” or “I aim to pay off my loans within 7 years instead of 15.” These clear targets will help you evaluate refinancing options and make decisions that truly serve your financial well-being.

What Should You Look for When Exploring Different Lender Options?

One of the key elements of a successful refinancing journey is finding the right lender. The lender you choose will not only determine the terms of your refinanced loan but also shape your repayment experience for years to come.

Begin by researching reputable lenders that specialize in student loan refinancing. Create a list of potential lenders and thoroughly evaluate each based on the following criteria:

Interest Rate Competitiveness: Compare both fixed and variable interest rates offered by different lenders. Remember that advertised rates typically represent the best possible scenario for highly qualified borrowers.

Available Loan Terms: Examine the range of repayment terms each lender offers. Some lenders provide terms as short as 5 years or as long as 20 years. Greater flexibility in term options allows you to better align your loan with your financial goals.

Fee Structure: Investigate whether lenders charge origination fees, application fees, prepayment penalties, or late payment fees. The good news? Many competitive refinancing lenders have eliminated most fees.

Borrower Protections and Benefits: Assess what happens if you experience financial hardship. Do they offer deferment or forbearance options? Do they provide death or disability discharge?

Customer Service Reputation: Research each lender’s customer service track record. Read reviews from current and former customers, check Better Business Bureau ratings, and explore complaints filed with the Consumer Financial Protection Bureau. A lender with responsive, helpful customer service can make your repayment experience much more pleasant.

Eligibility Requirements: Understand each lender’s qualification criteria, including minimum credit score, income requirements, and debt-to-income ratio thresholds. This will help you focus on lenders where you’re most likely to be approved and receive favorable terms.

Application Process: Consider the convenience and efficiency of each lender’s application process. Some offer streamlined applications with quick pre-qualification options that won’t affect your credit score. However, the fastest application process doesn’t guarantee the best rates, so it’s worth taking time to compare offers thoroughly.

Don’t hesitate to contact potential lenders directly with questions. Their responsiveness and willingness to address your concerns can provide insight into the service experience you might expect after refinancing.

Remember that refinancing is a long-term relationship. The lender offering the absolute lowest interest rate might not always be the best choice if they lack important borrower protections or have poor customer service. Similarly, the most convenient application process may not deliver the most competitive rates. Balance all factors—including rates, terms, service quality, and borrower protections—to find the lender that best meets your overall needs.

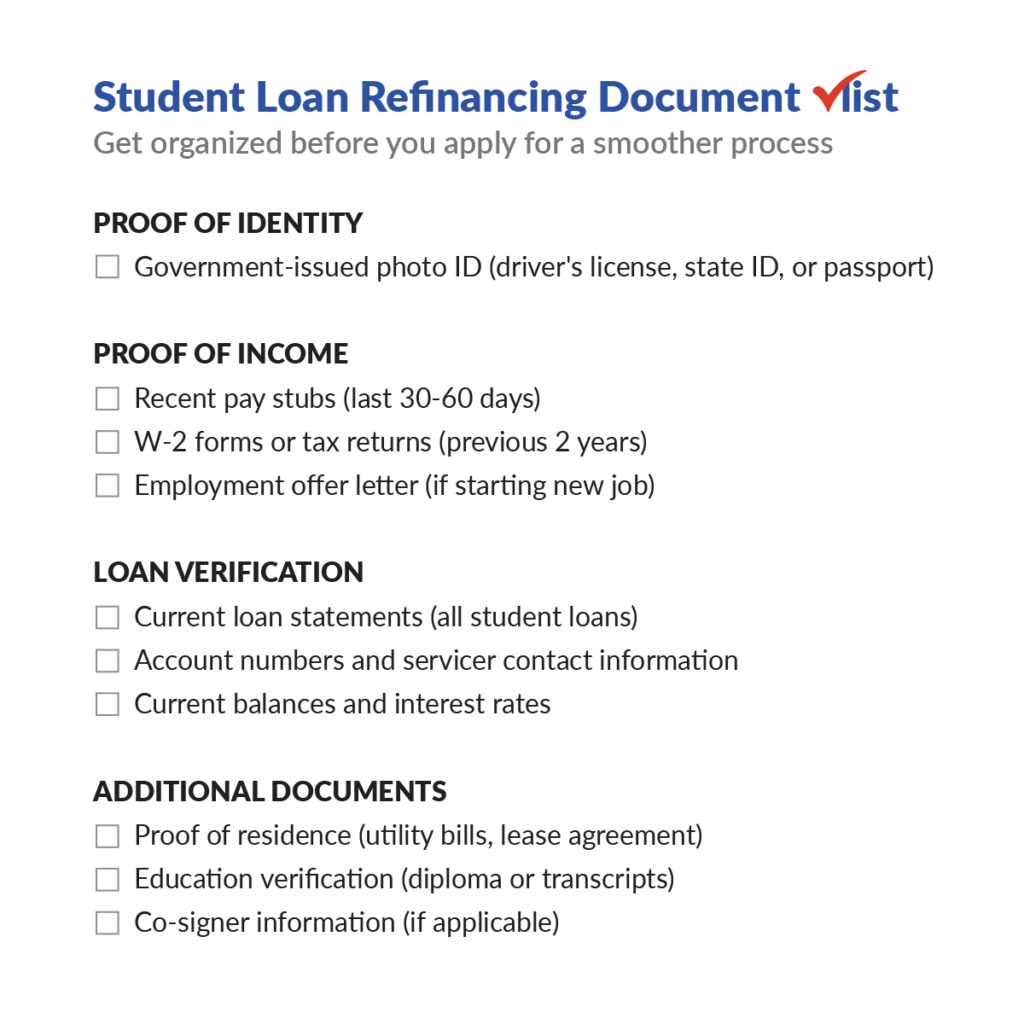

What Documentation Do You Need for a Smooth Application Process?

Once you’ve chosen a lender that aligns with your goals, it’s time to initiate the application process. Being well-prepared with the necessary documentation will streamline the process and potentially improve your chances of approval with favorable terms.

Typically, you’ll need to gather the following documents and information:

Proof of Identity: Government-issued photo identification such as a driver’s license, state ID, or passport to verify your identity and citizenship status.

Proof of Income: Recent pay stubs (usually from the last 30-60 days), W-2 forms, tax returns from the previous two years, or employment offer letters if you’re starting a new job. Self-employed borrowers may need to provide additional documentation such as profit and loss statements or business tax returns.

Loan Verification: Statements from all your current student loans showing account numbers, current balances, interest rates, and the contact information for your loan servicers. These documents help the new lender verify your existing loan details and ensure all loans are included in the refinancing process.

Credit Information: While you don’t need to provide your credit report (the lender will obtain this directly), it’s wise to review your credit report beforehand to ensure it’s accurate. Be prepared to explain any negative marks or discrepancies.

Proof of Residence: Utility bills, lease agreements, or mortgage statements that verify your current address.

Education Verification: Diploma or transcripts confirming your degree completion, especially if you’re a recent graduate.

Co-signer Information: If you’re applying with a co-signer, they will need to provide similar documentation regarding their identity, income, and residence.

Preparing these documents meticulously is essential to ensure a smooth application process. Organize them digitally (as many lenders prefer electronic submissions) and have physical copies available if needed. Complete all application forms thoroughly and accurately, as missing or incorrect information can delay the process or affect your approval odds.

Some lenders offer application checklists or pre-application consultations to help you gather everything needed before formally applying. Taking advantage of these resources can help you avoid common application pitfalls and expedite the process.

What Happens During the Approval Process and How Long Does It Take?

With your application submitted, the lender’s underwriting team will assess your eligibility and creditworthiness. Understanding this phase will help you navigate potential challenges and optimize your chances of approval.

The approval process typically involves several key steps:

Initial Application Review: The lender first reviews your application to ensure all required information has been provided and meets basic eligibility criteria.

Credit Check: The lender will conduct a formal credit inquiry to access your full credit report. They’ll evaluate your credit score, payment history, length of credit history, types of credit in use, and any negative marks such as late payments or collections.

Income and Employment Verification: Underwriters verify your employment status and income to ensure you have sufficient earnings to manage loan repayment. They may contact your employer directly to confirm your employment details.

Debt-to-Income (DTI) Ratio Assessment: Lenders calculate your DTI ratio by dividing your monthly debt obligations by your gross monthly income. A lower DTI ratio (typically below 50%) indicates better ability to take on new debt.

Education and Loan Verification: The underwriting team confirms your existing student loan details and verifies that your loans are eligible for refinancing.

The timeline for this process varies by lender, but you can generally expect:

- Initial application review and conditional approval: 1-10 business days

- Document verification and final underwriting: 1-2 weeks

- Final approval and loan offer: 2-4 weeks from initial application

- Loan disbursement (paying off existing loans): 2-6 weeks after accepting the offer

The key variables are lender efficiency, borrower responsiveness to document requests, and complexity of the existing loan situation. Some lenders have streamlined this process considerably, potentially reducing the timeline to as little as 10-15 days from application to disbursement. However, complications—missing documentation, employment verification challenges, or the need for a co-signer—can extend these timeframes. Your lender can provide a more specific timeline early in the process.

During this waiting period, you must continue making regular payments on your existing loans to avoid late fees and negatively affecting your credit score. Your obligation to your current loans remains until the refinancing process is complete and those loans are officially paid off by your new lender.

How Do You Evaluate Loan Offers and Make the Final Decision?

When evaluating loan offers, consider these important factors:

Interest Rate Comparison: Compare the interest rates offered against both your current rates and competing offers. Even small differences in interest rates can significantly impact your total cost over the life of the loan. Pay attention to whether rates are fixed (remaining constant throughout the loan term) or variable (fluctuating with market conditions). Remember that variable rates can rise significantly over time, potentially making a loan much more expensive than anticipated.

APR (Annual Percentage Rate): Look beyond the basic interest rate to the APR, which includes fees and provides a more comprehensive view of the loan’s cost. A loan with a slightly higher interest rate but no fees might have a lower APR than one with a lower rate but significant fees.

Monthly Payment Amount: Calculate how each offer affects your monthly budget. Will the new payment amount provide the financial relief you’re seeking, or is it structured to help you pay off the loan faster?

Total Cost of the Loan: Determine the total amount you’ll pay over the entire loan term (principal plus interest) for each offer. This figure reveals the true long-term cost of each option.

Loan Term Length: Evaluate how the repayment timeline aligns with your goals. A shorter term means higher monthly payments but less total interest paid over time. A longer term offers lower monthly payments but higher overall cost. However, if you’re currently trapped in high-rate loans, even a longer refinancing term at a significantly lower rate could reduce both your monthly payments and total interest costs.

Borrower Protections: Assess what safety nets each offer provides, such as forbearance options during financial hardship, disability discharge provisions, or flexible payment arrangements.

Prepayment Flexibility: Confirm there are no penalties for making extra payments or paying off the loan early, giving you the freedom to accelerate your debt payoff when possible.

Don’t rush this decision—take time to thoroughly understand each offer. If something is unclear, reach out to the lender for clarification. Remember that accepting a refinancing offer is a significant financial commitment that will impact your finances for years to come.

How Does INvestEd Guide You Through the Refinancing Process?

INvestEd is a dedicated partner, committed to ensuring that you navigate this path with confidence and clarity. In this section, we’ll illuminate the pivotal role that we play in guiding borrowers like you through the multifaceted world of refinancing student loans.

What Expert Guidance Does INvestEd Provide at Every Stage of Refinancing?

During the initial assessment phase, our experts conduct a review of your current loan portfolio, identifying opportunities for improvement and potential refinancing benefits specific to your situation. We analyze interest rates, loan terms, and special provisions of your existing loans, providing insights that might not be immediately apparent to those unfamiliar with the nuances of student loan structures.

Throughout the process, our specialists provide guidance on documentation requirements and application procedures, helping you present your financial profile in the most favorable light. We can help you understand how lenders evaluate applications and what factors might influence their decisions, allowing you to address potential concerns proactively.

We help you look beyond headline interest rates to understand the true cost and benefits of each offer, ensuring you make a well-informed decision that serves your long-term financial interests.

How Does INvestEd Help You Navigate the Complexities of Student Loan Refinancing?

Student loan refinancing—with its terms, conditions, and eligibility criteria—can often seem like a labyrinth. INvestEd’s role is to be your trusted map and compass, simplifying the complex and translating it into plain language. We’ll make sure that you not only understand each aspect of the refinancing process but also appreciate its implications for your financial future.

One of the most challenging aspects of refinancing is understanding the potential trade-offs, particularly when it comes to federal loan benefits. INvestEd provides clear explanations of what benefits you might forfeit when refinancing federal loans and helps you weigh these against the potential advantages of a new loan structure. We’ll help you navigate questions such as:

- How might refinancing affect your eligibility for income-driven repayment plans?

- What are the implications for potential loan forgiveness programs?

- How do deferment and forbearance options compare between your current loans and refinancing options?

- What impact might refinancing have on your tax situation?

We also help demystify complex terminology and loan features. Fixed versus variable interest rates, capitalized interest, loan amortization schedules—these concepts can be confusing even for financially savvy borrowers. INvestEd breaks down these terms into understandable components, ensuring you have a clear grasp of how each element affects your financial outcome.

How Can INvestEd Help You Maximize Financial Benefits Through Refinancing?

Whether your primary aim is to lower monthly payments, save money on interest, or expedite your debt-free journey, INvestEd will empower you to make choices that have a profound impact on your financial well-being.

With sophisticated analysis tools to quantify the potential impact of various refinancing scenarios, we provide personalized projections that illustrate exactly how different options might affect your financial situation both in the short term and over the life of your loan.

For borrowers primarily concerned with reducing monthly payments, we help identify lenders offering the most favorable combination of interest rates and term lengths to maximize monthly cash flow relief. We might recommend strategies such as extending the loan term while securing a lower interest rate, potentially reducing payments by hundreds of dollars each month.

If long-term savings is your priority, our experts focus on minimizing the total interest paid over the life of your loans. We help you explore options with the lowest possible interest rates, even if that means maintaining or slightly increasing your monthly payment. For many borrowers, this approach can yield savings of thousands or even tens of thousands of dollars.

For those eager to eliminate debt quickly, INvestEd can develop accelerated payoff strategies. Beyond simply identifying shorter-term refinancing options, we provide guidance on structuring your finances to make extra payments strategically, potentially shaving years off your repayment timeline without overextending your budget.

Why Is Personalized Decision-Making Support So Important When Refinancing?

Many borrowers feel overwhelmed when faced with multiple refinancing options and complex financial projections. In a state of such uncertainty, it’s easy to either make hasty decisions based on incomplete information or become paralyzed by indecision. Nobody wants that.

INvestEd provides a structured decision-making framework that helps you evaluate options methodically, considering both objective financial factors and your personal priorities. Our approach recognizes that the “best” refinancing option isn’t universal—it’s the one that aligns most closely with your unique circumstances and goals.

We help you develop clarity about your priorities by asking targeted questions and exploring hypothetical scenarios. For instance, if you’re unsure whether to prioritize lower monthly payments or long-term savings, we might illustrate how different approaches would affect your finances at various life stages or milestones.

Our support extends beyond numbers and calculations to address the emotional aspects of financial decision-making. We recognize that student loan debt can be a source of stress and anxiety for many borrowers. By providing reliable information, expert analysis, and a clear path forward, we help alleviate these concerns, allowing you to make decisions from a place of confidence rather than fear.

How Does INvestEd Provide Ongoing Support Throughout Your Financial Journey?

Our relationship with borrowers doesn’t end once refinancing is complete. We recognize that financial circumstances evolve, and the optimal strategy for managing your student loans may change over time. INvestEd provides ongoing support to help you navigate these changes and continue optimizing your approach to student debt management.

This continued support manifests in several important ways:

Regular Check-ins and Strategy Reviews: We can offer periodic reviews of your loan status and repayment progress, evaluating whether your current approach remains optimal or if adjustments might yield additional benefits. As your income grows, career changes, or major life events occur, we help you reassess your student loan strategy in the context of your evolving financial picture.

Guidance Through Financial Transitions: Major life changes such as career advancement, marriage, home purchase, or starting a family can significantly impact your financial priorities and capabilities. INvestEd can provide guidance on how to adjust your student loan management approach during these transitions, ensuring your repayment strategy remains aligned with your current circumstances.

Access to Continuing Education: Financial knowledge is constantly expanding, and new strategies for managing student debt emerge regularly. INvestEd provides access to updated information, webinars, and resources that keep you informed about developments that might benefit your situation.

Support During Financial Challenges: If you encounter unexpected financial difficulties that affect your ability to make loan payments, INvestEd can help you explore options such as temporary payment adjustments, hardship programs, or other alternatives to keep your financial plan on track during challenging periods.

Milestone Planning: As you approach significant debt reduction milestones or complete repayment, INvestEd helps you plan for the financial opportunities that emerge as your debt burden diminishes. We provide guidance on redirecting freed-up resources toward other financial goals such as retirement savings, investments, or major purchases.

Ready to Take a Major Step Toward Financial Freedom?

At INvestEd, we’re here to guide you through the student loan refinancing process with the same level of expert advice we’ve provided to thousands of Hoosier families for more than 45 years. Our team is truly invested in your financial success and can help you explore refinancing options that align with your unique goals.

Don’t let high interest rates hold you back any longer—connect with our friendly advisors today for a free, personalized consultation. With INvestEd by your side, you can make strong financial choices now that will benefit you for years to come.

Apply today and you can find out in two minutes how much you could be saving with a refinancing loan from INvestEd.Apply today and you can find out in two minutes how much you could be saving with a refinancing loan from INvestEd.